The Complete Guide to Trade Finance for Export Businesses

The world is now a truly global marketplace, with competition for business fierce.

The world is now a truly global marketplace, with competition for business fierce.

To grow your export business, you simply MUST be able to offer flexible finance and payment terms to your customers.

But…

You also have to make sure you get paid in full and on time.

Which is why the decision on which method of financing is appropriate for an individual export sale is critical to your business.

The transaction has to be attractive for the importer, but minimize (or preferably completely negate) risks of non payment for the exporter.

In this complete guide to trade finance we will start with an overview of the 4 major methods of payment for International trade, and then look at finance options available to exporters looking to grow their overseas business.

We will also look at a specific method of financing available to importers looking to bring in U.S. goods who are unable to raise finance through commercial banks.

To jump to a specific section you can use the links below:

- Chapter 1: Methods Of Payment In International Trade

- Chapter 2: Export Finance Options For Exporters

- Chapter 3: Non-Payment Risk Mitigation For Export Businesses

- Chapter 4: Government Assisted Foreign Buyer Financing (Ex-Im Bank)

Otherwise… let’s get started!

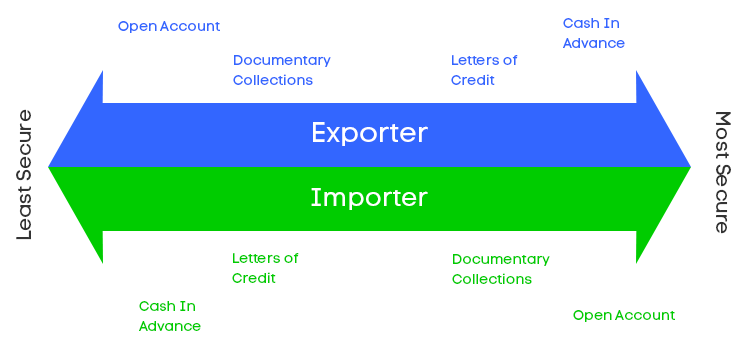

There are 4 major payment methods available for International trades:

- Cash In Advance

- Letters of Credit

- Documentary Collections

- Open Account

As the diagram below shows, the risks associated with each method are inverse for exporters and importers.

Now let’s take a closer look at each method, along with their advantages and associated risks.

The exporter gets payment up front from the buyer before shipping goods – normally by wire transfer or credit card.

Clearly this is attractive for the exporter as there is ZERO risk of non payment.

But for the buyer, there are 2 major issues:

- Cash flow – they have to lay out all the cash for the transaction before they have a chance to sell (or even receive) the goods

- Risk/Concerns – will the exporter actually ship the goods after payment?

It should be obvious that exporters who offer cash in advance as their only form of payment are at a serious disadvantage.

Frankly, if the customer can get credit terms for the same goods elsewhere, then you’re probably going to lose the sale.

Which means you’re going to miss out on making sales to a lot of high value, credit worthy businesses.

If cash in advance is the only available option, then the buyer may benefit from using a credit card to complete the transaction. However, as an exporter, be sure to check with the buyer’s credit card company for specific rules affecting international transactions and be wary of fraud.

When to consider using cash in advance terms:

- When the importer is a new customer/unestablished business

- When the importer’s creditworthiness is unverifiable, unsatisfactory, or in doubt

- When the political and commercial risks of the importer’s country are very high

- When your product is unique to your business (not available elsewhere) and has very high demand

- If you are operating an internet business and credit card (or wire payment) makes sense for convenience (both for the importer and exporter)

Letters of credit (LCs) are a common method of payment for international transactions.

In a nutshell, the buyer sets up an arrangement with their bank to release funds (guaranteed by the bank) when the terms of the trade have been met. Generally release of funds will require presentation of a set of required documents set out in the terms.

Letters of credit are particularly useful when the buyer represents an unsatisfactory credit risk for the exporter, but they are happy with the creditworthiness of the buyer’s foreign bank.

The buyer is protected as they do not have to pay for the goods until all terms of the agreement are met.

As LCs can be complicated arrangements, with lots of opportunity for discrepancy, they should only be prepared by expert documenters, or outsourced. Bare in mind that any discrepancy (however small) can be used as an excuse for non payment!

How A Letter of Credit Transaction Works

Here’s a quick illustration of how a typical Letter of Credit transaction works:

- The importer arranges for their issuing bank to open a Letter of Credit in the exporter’s favor

- The LC is transmitted by the issuing bank to the advising bank, which then forwards it to the exporter

- The goods are shipped out by the exporter to a freight forwarder, along with the documents

- The goods are dispatched by the freight forwarder and the documents are submitted (by them) to the advising bank

- The documents are checked by the advising bank for compliance with the LC, and if all is correct, the bank pays the exporter

- The importer’s account is debited by the issuing bank

- Documents are released by the issuing bank to allow the importer to claim their goods from the carrier

Types Of Letter of Credit

There are several types of Letter of Credit. Here is a quick overview of some of the most common forms.

Type 1: Irrevocable Letter of Credit

An irrevocable letter of credit can only be amended or cancelled after issuing if both parties (buyer and seller) agree.

Revocable letters of credit are rare, but are sometimes used when parent companies conduct international transactions with their subsidiaries.

When an LC is not clearly defined as either revocable or irrevocable ,it is automatically considered to be irrevocable.

Type 2: Confirmed Letter of Credit

Letters of Credit from foreign banks – particularly those from countries with an unstable political climate – present more risk to a US exporter.

This risk can be mitigated when the LC is confirmed (guaranteed) by a U.S. bank (the exporter’s advising bank).

Other (Special) Letters of Credit

- Transferable – The payment obligation for the LC can be transferred to one or more “second” beneficiaries

- Resolving – Credit is restored to its original amount by the issuing bank after it has been drawn down

- Standby – Can be used instead of security or deposit payments as a secondary form of payment

When a documentary collection is the set method of payment for an international transaction, the exporter passes collection of payment to their bank.

The exporter’s bank sends documents to a collecting bank (the importer’s) with instructions for payment.

This method of payment does not offer any real guarantees for the exporter, with limited recourse in the event of non-payment.

It is however (generally) a cheaper option than setting up a letter of credit for an export deal.

How A Documentary Collection Transaction Works

Here is an example of a typical documentary collection transaction:

- Goods are shipped out by the exporter and the documents are sent by the importer

- Documents are presented by the exporter to their bank along with instructions for obtaining payment

- The documents are sent by the exporter’s remitting bank to the importer’s collecting bank

- Documents are released to the importer by the collecting bank on receipt of payment

- Alternatively, the collecting bank may release the documents on acceptance of a draft from the importer

- After release of documents, the importer can present them to the carrier and take receipt of the goods

- Payment is forwarded by the collecting bank to the remitting bank

- The remitting bank credits the exporter’s account

Types of Documentary Collection Transactions

There are 2 major types of documentary collection transaction:

Documents Against Payment (D/P) Collection

The exporter ships the goods and then forwards documents to their bank. The documents are forwarded to the importer’s collecting bank (with instructions for payment) and the documents are released upon receipt of full payment.

Documents Against Acceptance (D/A) Collection

This method of payment involves extending credit of sorts to the importer. The credit takes the form of a ‘time draft’, which is a legal obligation for the importer to pay for the goods at a future date.

When the date is reached, the collecting bank contacts the importer for payment, and forwards the funds to the remitting bank for credit to the exporter’s account.

Open account is basically extending credit (exporter) to the customer (importer). Payment terms are usually set to between 30 and 90 days after delivery of goods.

Clearly this is great for the buyer: they get the goods and have a period to make sales to cover their costs of purchase. They therefore don’t have to dip into their existing cash flow or reserves to import goods.

It is of course however, the highest risk option for the exporter. They ship the goods, wait for the agreed period, and are reliant on the customer stumping up the cash on the agreed date.

Fortunately, there are various finance options available for exporters to offer open account terms to their overseas customers. These can be combined with insurance and other products to negate risk of non-payment.

In chapter 2, we will look at these finance options in more detail, before moving on to look at methods of mitigating risk of non-payment.

It’s clear that to win customers in competitive export markets, your business should offer attractive (and flexible) payment terms. And as we have already seen, open account (or credit) terms are the most beneficial for importers.

To help your export business to grow, there are a number of solutions available – all of which will allow you to extend credit, and some which will also help to finance your capital equipment/stock.

Here is an overview of each option.

Export working capital is finance provided by a commercial bank to help support export sales.

Funds can be provided for purchasing the goods and services required for exporting, and also for easing cash flow to allow exporters to offer credit terms to their customers.

An export working capital facility can be set up to finance an individual deal, or alternatively a general facility can be agreed to finance multiple export sales.

For individual transactions, the facility will normally have a one year term, while general facilities may be extended for up to three years.

How To Qualify For Export Working Capital Financing

To qualify for export working capital financing from a commercial bank, an exporter will have to demonstrate:

a) profitability

b) a need for the facility

c) that a viable transaction (export deal) is in place

Depending on the risk, the bank may ask for a security against the finance. This will normally be a charge over the company’s assets, or in some cases a personal guarantee.

It is also standard practice for the bank to collect receivables directly from the customer, deducting any fees, and passing the balance to the exporter.

Types of Export Working Capital Finance

Here is an overview of the 2 types of export working finance available:

Transaction Specific

Generally a transaction specific loan will be short term and taken out to cover a large, or atypical export order. The term of the loan will normally be between 3 and 12 months, with interest rates generally fixed over the period.

Revolving Credit

A revolving line of credit is appropriate for a business who wishes to have a level of financial comfort to enable them to complete regular export deals. This is the best option for export companies who do not have a predictable order book and may have peaks and troughs in their business.

Funds can be drawn down to the agreed level at any time while the agreement remains in place.

In some cases a government guarantee may be required to access finance (see below).

In cases where commercial banks are reluctant to lend, or borrowing limits are insufficient to meet requirements, the U.S. government has a guarantee scheme available to help exporters get access to the finance they need.

The Export-Import Bank of the United States (Ex-Im Bank) and the U.S. Small Business Administration (SBA) work together to provide finance to export businesses through participating lenders.

Typically the SBA will handle finance requirements below $2 million (and support is limited to small businesses), while Ex-Im will assist with larger facilities.

These government backed loans are known as ‘Government-Guaranteed Export Working Capital Programs (EWCP)’ and allow export businesses to borrow more against their total collateral value than non-guaranteed loans.

This illustration from the US trade department shows how a loan backed by an EWCP allows a business to borrow more than double the amount they would with a non-guaranteed loan.

Here is a breakdown of the key features of the two options:

Ex-Im Bank Guaranteed Loans

- Available to US export businesses

- Access to large lines of credit – generally upwards of $2 million

- $100 application fee

- One year loan subject to 1.5 percent upfront fee (total loan amount)

- Commercial lender fees and interest rates negotiable

- Special deals available to minority, women owned, rural and environmental firms

- Not generally available for military use and certain countries may be restricted

SBA Guaranteed Loans

- Available to small export businesses that meet SBA guidelines

- Credit lines up to $2 million

- No restrictions on countries or military sales

- No application fees

- 1 year loan subject to 0.25 percent upfront fee

- Commercial lender fees and interest rates negotiable

For protection from risk of non-payment when offering open account terms, export finance should be combined with a risk mitigation option. Below we will look at 3 of the most effective solutions for risk mitigation.

Export credit insurance protects an exporter against the risks of non-payment in an International transaction.

With the right export credit insurance policy in place an exporter will be covered against:

- Buyer insolvency

- Buyer bankruptcy or default

- Political risks (war, terrorism, riots, revolution etc)

- Fluctuations in currency

Export credit insurance can be taken out on a single policy basis (against a single transaction), or a general policy can be sought to cover multiple export deals.

Policies can cover both short term transactions (up to one year) and medium term payment options (one to five years).

Advantages of Export Credit Insurance

- Minimizes the risk of non-payment and allows export businesses to provide competitive open account terms to foreign buyers

- Allows export businesses to expand into emerging markets, which may be classed as a higher credit risk

- Having insurance in place for foreign receivables will give banks increased comfort in lending

Export Credit Insurance Coverage

A short term policy will generally insure between 90 and 95 percent of the transaction value against non-payment.

Consumer goods and services are normally covered for up to 180 days, while small capital goods, consumer durables and bulk commodities can be covered for up to 360 days.

Medium term export credit insurance generally provides 85 percent coverage on large capital equipment transactions for up to 5 years.

Export Credit Insurance Costs

The cost of a particular export credit insurance policy will depend on a number of factors, including:

- The creditworthiness of the importer

- The size of the transaction

- The exporter’s commercial experience

While most general (multi-transaction) policies will cost less than 1 percent of total insured sales value, individual transaction policies will fluctuate depending on the above factors.

Regardless, the cost of taking out an ECI policy should be significantly less than the costs associated with setting up a letter of credit transaction.

Ex-Im Bank Credit Insurance

We recommend taking out an export credit insurance policy from Ex-Im Bank.

Ex-Im is able to provide coverage in emerging markets, which may not be available through private insurance companies.

Additionally Ex-Im policies are backed by the credit of the U.S. government (it doesn’t get more sound than that!) and exporters buying multiple policies can benefit from significant discounts on their premiums.

Yegg Inc is a licensed broker (registered with Ex-Im Bank) of Export Credit Insurance and can assist your business in putting an appropriate policy in place. Find out more about our Ex-Im Bank export credit insurance services here.

Export Factoring is a complete, all-in-one solution for exporters which combines:

- Working capital financing

- Credit protection

- Foreign accounts receivable bookkeeping

- Collection of accounts receivable

A factor purchases an exporter’s short-term foreign receivables at a discount from book value and assumes all collection responsibilities and risks of non-payment.

Clearly this protects an exporter 100% from payment default, however, as the book value is discounted, this option is more expensive than export credit insurance.

Generally factoring is most beneficial for businesses who are experiencing rapid growth in their export sales, as cash for exports come in up front (although at a discount) allowing investment in additional stock.

Typical Export Factoring Arrangements

There are two main types of export factoring arrangement.

Discount Factoring

The factor pays the exporter an advance of funds against their foreign receivables until the cash is collected from the importer.

Collection Factoring

The exporter is paid the value of the sale (minus a commission charge) when receivables fall due. The cost of the commission can be anywhere between 1 and 4 percent depending on the risk to the factor.

Disadvantages Of Export Factoring

- Certain countries have laws which forbid the selling of receivables

- Generally only available on short term, open account receivables (up to 180 days)

- Costs are normally higher than with other options such as export credit insurance

Yegg Inc can help set up an export factoring solution tailored to your business requirements. Contact us for more information.

Forfaiting is similar to export factoring, in that foreign receivables are sold to a third party. However, unlike factoring it can be used to finance medium-long term transactions (payment terms up to 7 years).

Receivables are normally guaranteed by the importers bank, allowing the exporter to take the transaction off their balance sheet and have comfort on receiving payment.

The minimum transaction value for forfaiting is currently set at $100,000.

Advantages of Forfaiting

- 100% financing of contract value – completely eliminating risk of non payment

- Allows exporter to offer open account terms for large deals in high risk markets

- Exporter gains a guarantee from the importer’s bank

- Interest rate is generally fixed for the term

Disadvantages of Forfaiting

- Costs are generally higher than commercial bank financing

- Limited to transactions over $100,000

Example of a Typical International Trade Using Forfaiting

- The exporter approaches a forfaiter before finalizing details of their international transaction

- The forfaiter agrees to the deal and sets a ‘discount rate’ (their commission)

- Guarantees are obtained from the importer’s bank to complete the forfaiting

- The exporter delivers the goods to the importer

- Documents are delivered to and verified by the forfaiter

- Payment is made by the forfaiter to the exporter as agreed in the original contract

- Collection responsibility rests with the forfaiter

Yegg Inc can arrange forfaiting for your International trade. Contact us for more information.

")

For large export deals, involving high value goods, commercial bank funding may be unavailable or difficult to secure for foreign buyers. Particularly if they are located in a developing, or politically unstable country.

In these cases it is worth exploring government assisted foreign buyer financing from Ex-Im Bank.

Ex-Im Bank will assist with financing for creditworthy foreign buyers when they are purchasing U.S. goods and services from U.S. businesses.

While the bank does not directly compete with the commercial banking sector, it is there to ‘fill the gap’ when suitable funding cannot be found.

Advantages of Government Assisted Foreign Buyer Financing

- No maximum or minimum transaction value

- Financing available to creditworthy importers from developing and politically unstable countries

- Repayment terms up to 5 years for exports of capital goods and services (15 percent deposit required)

- Repayment terms up to 10 years for transportation equipment and large scale projects (some projects may qualify for up to 15 years financing)

- Negotiated interest rate

- Fast documentation process

Disadvantages of Government Assisted Foreign Buyer Financing

- Military items excluded

- Goods must meet Ex-Im’s foreign content requirements

- Not available in certain countries and subject to U.S. foreign policy

If you are an international importer looking to finance a purchase from a U.S. business and wish to apply for Ex-Im Bank funding please contact us for assistance.

Finding The Right Trade Finance Solution For Your Business

Every business is unique and, as you will have seen, there are a number of factors to consider when choosing a trade finance solution (or combination of solutions) for your business.

If you need assistance with finding the right finance for your company, or with setting up any of the options then we can help.

Contact us to discuss your specific requirements and we’ll help you find and implement the best solution for growing your export or import business.

And if you have any questions regarding this guide, then please leave a comment below and we’ll be happy to assist!